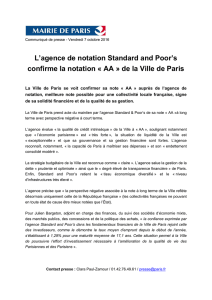

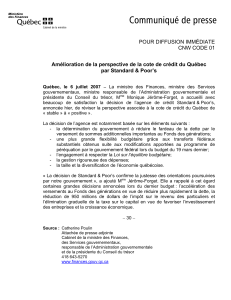

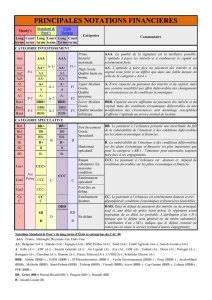

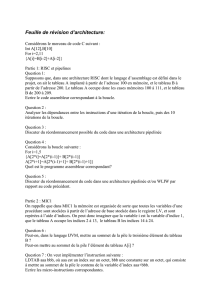

Les Critères de notation bancaire

Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Copyright © 2012 Standard & Poor’s Financial Services LLC, a subsidiary of The McGraw-Hill Companies, Inc. All rights reserved.

Les Critères de notation bancaire

Bernard de Longevialle

Responsable de la notation des banques & assurances pour la zone EEMEA &

Russie CEI (Communauté des Etats indépendants)

Notations - Institutions Financières

Avril 2012

2. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Agenda

•Notre nouvelle méthodologie: Une interconnexion accrue entre

les notes souveraines et bancaires

–Analyse des risques de l’industrie bancaire et de l’économie (BICRA)

–Facteurs spécifiques à la banque

–Soutien externe

•Tendances des notations en France et en Europe

3. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Critères de notation bancaire

4. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

Bank Ratings Framework

Méthodologie

BICRA

Score BICRA

Evaluation du

risque de

l’industrie et de

l’économie

Méthodologie

bancaire

Facteurs macro

économiques Facteurs de notations

propres à la banque Soutien externe

Ancre SACP

Analyse

intrinsèque

ICR

Note de

crédit de

l’émetteur

Notation de la dette

hybride et des

actions de

préférence

Notation de la

dette senior non

sécurisée

Risque de l’économie

Risque de l’industrie

Soutien du

groupe

Soutien du

gouvernement

Profil de

l’activité

Capital et

rentabilité

Profil de

risque

Financement

et liquidité

5. Permission to reprint or distribute any content from this presentation requires the prior written approval of Standard & Poor’s.

BICRA: Analyse du risque économique et du risque

liéàl’industrie

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

1

/

24

100%